U.S. Control For Canada's Sherritt And Cuba's Nickel/Cobalt? Ray Washburne, First Trump Administration OPIC President & CEO And Current Chairman Of Sunoco LLC Making An Offer?

/DiscoveryAlert.com

By Muflih Hidayat

Sherritt Cuba Mining Deal: Ex-Trump Adviser’s Bold 2026 Bid

When Political Capital Becomes Mining Capital: The Sherritt Cuba Deal Explained

Few industries illustrate the intersection of geopolitics and commodity markets as vividly as mining in sanctioned jurisdictions. The Sherritt Cuba mining business ex-Trump adviser transaction now taking shape represents one of the most unusual episodes in modern mining history. For decades, Western companies operating in countries subject to US sanctions have constructed elaborate corporate architectures, navigated shifting diplomatic winds, and absorbed significant financial penalties to maintain access to mineral deposits that are simply too strategically valuable to abandon.

Understanding Sherritt's Cuban Operations and Why They Matter

To understand what is currently at stake, it is essential to first appreciate the depth of Sherritt International's Cuban footprint. The Toronto-headquartered company has spent roughly three decades building one of the most geopolitically exposed mining portfolios in the Western Hemisphere, centred on Cuba's Moa district, which hosts one of the most significant laterite nickel-cobalt deposits outside of the Democratic Republic of Congo.

The core of Sherritt's Cuba business revolves around three interlocking asset positions: Asset Ownership Structure Primary Output

Moa Joint Venture 50% (alongside Cuban state partner) Nickel and cobalt

Energas One-third interest Natural gas and independent power generation

Downstream Refining Integrated processing capacity Finished nickel and cobalt metal products

What makes this portfolio simultaneously valuable and problematic is a single, decades-old carve-out: the United States market remains entirely inaccessible to Sherritt's products, a direct consequence of the sanctions framework that has governed US-Cuba relations since the 1960s. This restriction has shaped every financing decision, every offtake arrangement, and every capital raise Sherritt has executed in its Cuban business life.

The Geological Case for Moa's Strategic Importance

The Moa nickel-cobalt laterite deposit deserves particular attention from a geological perspective. Laterite deposits form through long-term tropical weathering of ultramafic rocks, typically peridotite or serpentinite, producing surface and near-surface concentrations of nickel and cobalt in oxidised mineral forms. The Moa district's ore is primarily processed through High Pressure Acid Leach (HPAL) technology, an energy-intensive hydrometallurgical method that dissolves nickel and cobalt from the ore under high temperature and pressure conditions using concentrated sulfuric acid.

HPAL is the preferred processing route for laterite ores globally because it achieves high recovery rates, typically in the range of 85-90% for nickel and 75-80% for cobalt, but it demands enormous energy inputs at the processing plant level. This technical dependency on consistent, high-volume electricity supply is precisely why Cuba's ongoing energy crisis has been so damaging to Sherritt's operational throughput. The Moa facility requires approximately 120 megawatts of consistent electrical supply to maintain full processing capacity, a level of demand that Cuba's chronically unstable national grid has increasingly struggled to provide.

From a battery metals supply chain perspective, Cuba's cobalt output carries particular strategic weight. Cobalt is a critical cathode material in lithium-ion battery chemistries used across the electric vehicle sector. Furthermore, the critical minerals demand driving the global energy transition has intensified scrutiny of every significant non-African cobalt source, and Cuba represents one of the very few available to Western battery manufacturers seeking geographic supply diversification.

Cuba's Energy Crisis and Its Cascading Impact on Moa

Cuba's deteriorating energy infrastructure has created a compounding operational challenge for Sherritt that extends well beyond simple power interruptions. Fuel supply constraints have forced repeated reductions in HPAL plant throughput, affecting both nickel and cobalt recovery volumes. The island's petroleum supply situation, which worsened significantly after 2019 and has continued to deteriorate through the mid-2020s, has created cascading disruptions across Cuba's entire industrial sector.

Sherritt's response to these challenges has included energy efficiency investments and partial operational deferrals, but the fundamental constraint — inadequate and unreliable electricity supply at the Moa site — cannot be resolved through operational adjustments alone. This context matters enormously when assessing the Gillon Capital transaction, because any new controlling shareholder would inherit not just the legal sanctions exposure but also an operationally constrained asset in a jurisdiction where the host government itself is struggling to maintain basic infrastructure.

The Helms-Burton Act: A 1990s Law With 2026 Consequences

The legal architecture that has defined Sherritt's relationship with the United States market traces back to a piece of 1996 legislation that codified decades of Cuban embargo policy into federal statute. The Cuban Liberty and Democratic Solidarity (Libertad) Act, universally known as the Helms-Burton Act, was enacted in February 1996 and represented one of the most aggressive extraterritorial applications of US sanctions law in history.

The legislation operates through several mechanisms, but the most consequential for foreign mining companies is Title III, which grants US nationals the right to pursue civil litigation in US federal courts against any foreign person or entity that knowingly traffics in property confiscated by the Cuban government after January 1, 1959. For Sherritt, whose Cuban operations sit directly on assets that fall squarely within this definition, the exposure has been real and persistent.

The practical consequences for Sherritt over the decades have included: Permanent exclusion from US capital markets and US dollar financing channels:

Inability to engage with US-listed institutional investors in the company's equity; Individual executives historically being barred from entering the United States; Restriction from selling nickel and cobalt products to US-based buyers; Severely limited access to US banking relationships and clearing systems

The Helms-Burton Act's Title III provision enables US nationals to pursue civil legal action against foreign companies operating on formerly American-owned Cuban assets, a mechanism that has placed Sherritt under persistent legal and financial pressure since the late 1990s. The Trump administration's decision in 2019 to activate Title III after years of presidential waivers significantly escalated this exposure.

Sherritt's historical response to this environment involved constructing an offshore subsidiary architecture using entities registered in Barbados, which served as legal intermediaries between the Toronto-listed parent and the Cuban operating entities. However, this buffer has become increasingly inadequate as US sanctions enforcement has grown more sophisticated and aggressive. The critical minerals tariff landscape has, in addition, layered further complexity onto the already strained compliance environment.

The Executive Order That Triggered Corporate Collapse

In May 2026, President Trump signed an executive order that fundamentally altered the sanctions calculus for Sherritt. Unlike the Helms-Burton framework, which targeted companies based on their historical engagement with confiscated properties, the new order broadened punitive reach to a wider class of foreign corporate actors conducting any form of business in Cuba, extending the sanctions perimeter in ways that made Sherritt's existing offshore structures legally untenable.

The immediate corporate fallout was severe: Three board members resigned in rapid succession, reflecting the depth of concern about personal liability exposure; The Chief Financial Officer departed the company, removing a key financial leadership figure at a moment of acute crisis; Sherritt's share price, already trading at penny stock levels, collapsed sharply following the announcement; Management announced plans to relinquish its 50% stake in the Moa Joint Venture and surrender the Energas interest entirely; Then, within days of announcing a full withdrawal, Sherritt reversed course. The company disclosed it was evaluating what it described as a potential value-preserving opportunity, language that foreshadowed the Gillon Capital transaction now under negotiation.

The logic of reversal is instructive. Outright abandonment of assets in a sanctioned jurisdiction is not as simple as it sounds. Cuban state partners hold co-ownership positions that complicate unilateral exit. Furthermore, a structured ownership transfer to a party with US political connectivity offered a potentially cleaner pathway than unilateral dissolution, particularly if that transfer could be structured with explicit non-objection from US regulatory authorities.

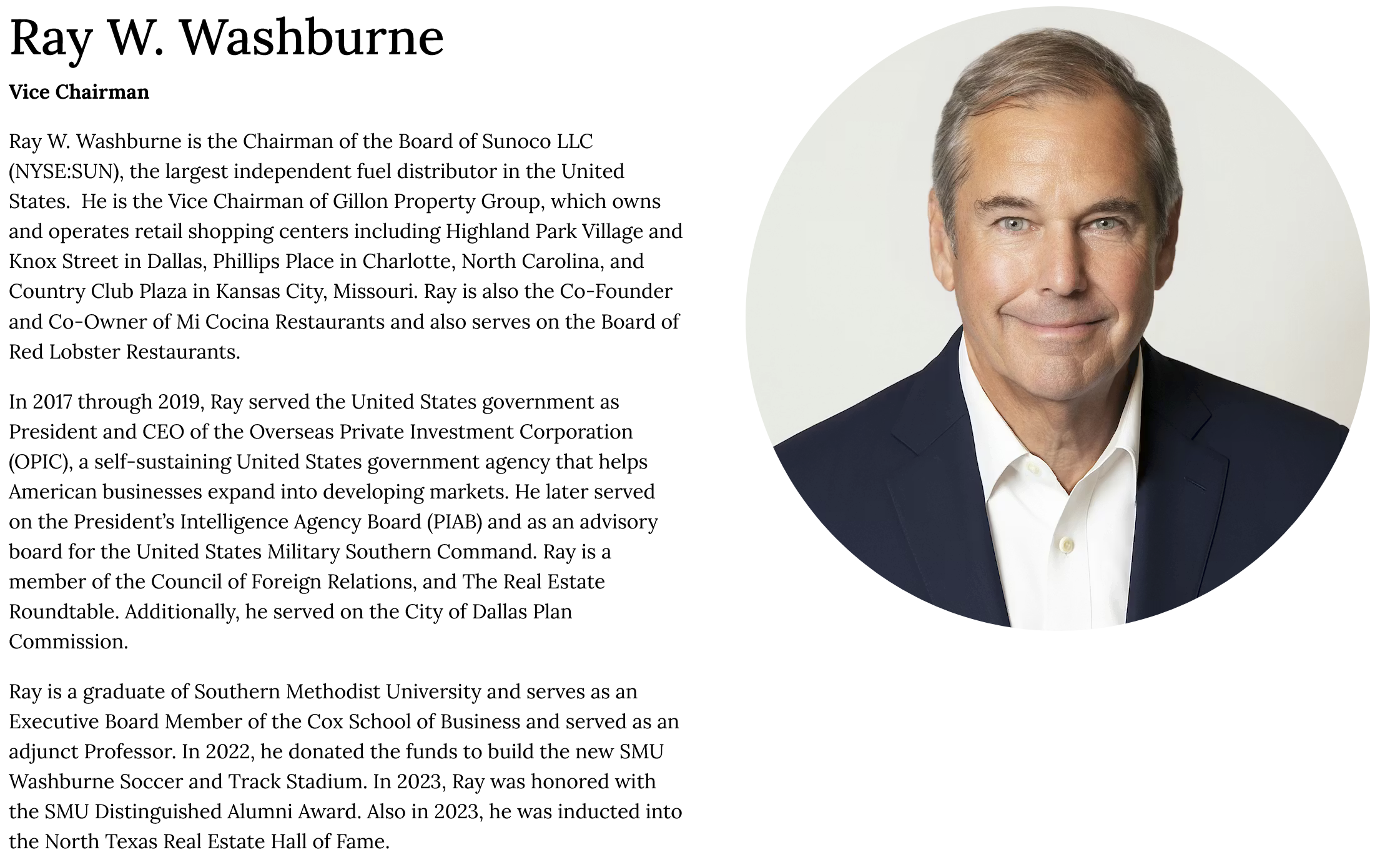

Ray Washburne and the Political Calculus of Gillon Capital

The identity of the acquiring party is arguably the most unusual element of this transaction. Ray Washburne is a Texas-based real estate executive whose public profile was significantly elevated during the first Trump administration, when his government roles placed him at the intersection of US development finance and executive branch intelligence advisory functions.

Role Appointing Authority Institutional Significance

Head, Overseas Private Investment Corporation (OPIC) President Trump, 2017 Oversaw US government development finance and political risk insurance globally, Member, Presidential Intelligence Advisory Board President Trump Senior advisory role with direct access to intelligence community briefings

Washburne operates through Gillon Capital LLC, a family office investment vehicle through which he has structured the proposed Sherritt transaction.

The OPIC connection deserves particular attention because it is not merely biographical colour. OPIC, now restructured as the US International Development Finance Corporation (DFC), exists precisely to deploy capital into politically complex, high-risk jurisdictions where conventional private capital is reluctant to operate. Its toolset includes political risk insurance, loan guarantees, and equity co-investments specifically designed for environments characterised by sovereign instability, sanctions risk, and state-partner complexity.

An executive with institutional knowledge of OPIC's operational frameworks would possess unusually relevant expertise for navigating exactly the kind of environment that defines the Sherritt Cuba mining business ex-Trump adviser transaction. Consequently, this is not incidental — the situation combines sovereign co-ownership dynamics, active sanctions exposure, and operational risk in a politically closed economy in ways that mirror the types of transactions OPIC was specifically built to evaluate.

Deal Structure: How the Warrant-Based Transaction Works

The mechanics of the proposed transaction reflect a sophisticated approach to managing regulatory and valuation uncertainty. Rather than a straightforward share acquisition, the deal is structured around a warrant-based private placement, a mechanism that has specific advantages in the current context.

The key structural parameters disclosed by Sherritt include: Instrument: Warrant-based private placement (not direct share purchase); Target ownership: Gillon Capital would acquire sufficient common shares to reach 55% of Sherritt on a fully exercised basis; Exercise price: Expected to be set at a discount to Sherritt's May 15, 2026 closing price; Market reaction: Sherritt shares rose approximately 9% in early New York trading following the announcement.

The warrant structure serves several functions simultaneously. First, it allows Gillon Capital to stage its economic commitment, preserving optionality if regulatory conditions shift. Second, it allows the transaction to proceed without requiring immediate full payment, giving both parties time to navigate the regulatory engagement process. Third, the discount to the May 15 closing price provides Gillon Capital a margin of safety given the share price volatility that preceded and followed the executive order shock.

What US Government Non-Objection Actually Means

Sherritt confirmed that it has engaged constructively with the US Department of State, which confirmed no objections to Gillon Capital's engagement. Both the Department of State and the Department of Treasury have indicated they do not view the current negotiations as contrary to US law.

A statement of non-objection from the State Department and Treasury is not a formal sanctions licence or legal clearance. It represents a preliminary signal that the transaction structure, as currently described, does not appear to conflict with existing US sanctions regulations. The distinction matters significantly for ongoing due diligence and deal execution risk assessment.

The critical regulatory institution in this context is the Office of Foreign Assets Control (OFAC) at the US Treasury, which administers and enforces economic and trade sanctions. The non-objection signals from State and Treasury suggest preliminary regulatory alignment, not a concluded compliance determination. The broader geopolitical mining landscape in 2025 and 2026 has, however, shown that such preliminary alignments can shift rapidly as political priorities evolve.

Precedents: When Political Ownership Restructuring Has Been Used Before

The Sherritt situation is unusual but not entirely without precedent. Several historical cases illustrate how ownership restructuring has been deployed as a mechanism to resolve sanctions complications in extractive industries:

Rusal and EN+ (2018-2019): Following OFAC sanctions on Russian oligarch Oleg Deripaska, the world's second-largest aluminium producer underwent a complex ownership restructuring specifically designed to dilute Deripaska's control below sanctionable ownership thresholds. The restructuring ultimately achieved sanctions removal through negotiated equity dilution.

Vedanta and Zambia Copper (2023): Government-driven restructuring of a major copper producer in a politically sensitive African jurisdiction demonstrated how sovereign co-ownership dynamics can reshape foreign-controlled mining ventures under pressure, with the host state ultimately exercising disproportionate influence over the outcome.

Turquoise Hill and the Oyu Tolgoi Structure: The lengthy dispute between Rio Tinto, Turquoise Hill, and the Mongolian government over the Oyu Tolgoi copper-gold mine illustrated how minority sovereign partners can exercise veto power over operational and ownership decisions far beyond what their equity percentage would suggest, particularly when the host state views the asset as nationally strategic.

The lesson across all three cases is consistent: the legal mechanics of ownership transfer are secondary to the willingness of the host sovereign to accept the new ownership configuration. In the Sherritt context, this means Cuban state acceptance of US-connected controlling ownership is the most important variable in the entire transaction.

Key Risks That Could Prevent Deal Completion

Investors and observers evaluating this transaction should weigh a differentiated risk matrix rather than treating US regulatory non-objection as the primary variable:

Risk Category Description Assessment

Cuban state consent The Cuban government may resist or complicate foreign ownership restructuring involving US-connected parties Structurally complex, no clear precedent

US policy reversal Sanctions posture shifts before warrants are exercised Medium, dependent on Trump administration policy continuity

Operational deterioration Continued fuel constraints reduce asset value before deal closes Medium-High given existing trajectory

Helms-Burton third-party claims Independent claimants may pursue Title III litigation regardless of ownership change Medium, structurally independent of transaction

Warrant pricing disputes Share price movements may create disagreements over exercise price calculations Lower probability but possible

The Cuban sovereign partner dynamic deserves emphasis because it is the risk that receives the least analytical attention relative to its actual importance. Cuba accepting a US-connected entity as the controlling shareholder of its primary foreign mining partner would represent a geopolitically extraordinary decision. Whether the Cuban government views the Gillon Capital transaction as acceptable pragmatism or unacceptable encroachment will likely prove more determinative than any US regulatory outcome.

Battery Metals Implications: What a Sherritt Ownership Change Means for Supply Chains

Beyond the corporate drama, the Sherritt situation carries genuine implications for global battery metals supply chains. Cuba's Moa district is one of the Western Hemisphere's most significant sources of Class I nickel and cobalt, and the trajectory of its ownership matters to anyone tracking critical mineral supply diversification. In addition, global cobalt production remains heavily concentrated in the Democratic Republic of Congo, making alternative sources like Moa strategically significant.

If the Gillon Capital transaction closes and a US-connected controlling owner stabilises Sherritt's Cuban operations, several supply chain dynamics could shift: Previously inaccessible US capital markets could potentially become available for operational investment, addressing the chronic undercapitalisation that has contributed to production declines; Technology partnerships with US-based engineering and process improvement companies, currently restricted by sanctions, could theoretically become accessible; Offtake arrangements with US battery manufacturers or their supply chain partners might become structurally possible for the first time; Cuban cobalt would gain a clearer pathway toward qualifying as a non-DRC source for Western battery manufacturers seeking to reduce supply chain concentration.

However, Cuban state co-ownership of the Moa Joint Venture means none of these potential changes flow automatically from a Sherritt-level ownership restructuring. Every material operational change would still require Cuban state partner engagement and approval.

Three Scenarios for Sherritt's Future

Scenario 1: Deal Closes, US-Connected Ownership Stabilises Operations. Gillon Capital exercises its warrants, acquires 55% control, and leverages Washington relationships to negotiate a durable operating framework. Cuban state partners accept the new configuration on pragmatic economic grounds. Moa output stabilises as capital access improves and operational investment resumes.

Scenario 2: Deal Stalls, Exit Planning Resumes. Regulatory complications, Cuban sovereign resistance, or warrant pricing disputes prevent deal closure. Sherritt reverts to its original exit strategy, triggering renewed share price pressure and potential asset write-downs in a jurisdiction where recovery of asset value through conventional legal mechanisms is structurally improbable.

Scenario 3: Partial Transaction, Hybrid Ownership Emerges. Warrants are partially exercised, creating a minority US-connected position without full control transfer. This hybrid outcome preserves optionality for all parties while leaving the fundamental sanctions exposure unresolved and creating a structurally ambiguous arrangement that satisfies neither the US regulatory agenda nor the Cuban state's interest in a stable, committed foreign partner.

The trade war impacts of 2025 have, furthermore, demonstrated that geopolitically motivated corporate restructurings are increasingly common in extractive industries, as companies seek to reposition assets along politically acceptable ownership lines. The Sherritt Cuba mining business ex-Trump adviser deal is, in many respects, a product of this broader realignment.

This unique situation is examined in further detail by the Financial Post, which has tracked the evolving sanctions calculus and corporate response throughout 2026.

The Sherritt-Gillon Capital transaction is less a conventional mining acquisition and more a geopolitical arbitrage attempt- an effort to use political connectivity to transform what has been an intractable sanctions problem into a manageable regulatory relationship. Whether that transformation proves achievable depends as much on calculations being made in Havana as on signals emanating from Washington.

CU-2619: MOA Bay Mining Company, Improved Real Property, Oriente, Republic of Cuba, US$88,349,000.00. Link To Claim Filing In PDF Format

Association for the Study of the Cuban Economy: A further example of the accounting and legal complexities that will be involved in Cuban settlements is the case of Moa Bay Mining Company, which claimed $88.3 million in confiscation losses. The company was wholly owned by Freeport Nickel Company, a subsidiary of Freeport Sulphur Corporation. Freeport Sulphur merged with McMoRan Oil & Gas, LLC in 1998 but remained a wholly owned subsidiary of the successor company McMoRan Exploration Co. (“McMoRan”). In 2002, McMoRan sold Freeport to a 50–50 joint venture between IMC Global Inc.—the world’s largest purchaser and user of sulphur—and Savage Industries Inc., a major materials management and transportation systems company. The possible compensation for Moa Bay’s Cuban assets should be of interest to IMC and Savage, as the current value of the confiscated nickel and cobalt mines is estimated at $5–7 billion. Since 1990, Canada’s Sherritt International has invested over half a billion dollars in Freeport’s former mines under a joint venture with the Cuban government, and China is negotiating a similar joint venture. Cuban nickel is considered to be Class II with an average 90 percent nickel plus content. Holguín Province, where the Moa Bay mines are located, is estimated to contain 34 percent of the world’s known reserves of nickel, or some 800 million tons of proven nickel plus cobalt reserves, and another 2.2 billion tons of probable reserves.

Libertad Act

The Trump Administration has made operational Title III and further implemented Title IV of the Cuban Liberty and Democratic Solidarity Act of 1996 (known as “Libertad Act”).

Title III authorizes lawsuits in United States District Courts against companies and individuals who are using a certified claim or non-certified claim where the owner of the certified claim or non-certified claim has not received compensation from the Republic of Cuba or from a third-party who is using (“trafficking”) the asset.

Title IV restricts entry into the United States by individuals who have connectivity to unresolved certified claims or non-certified claims. One Canada-based company and one Spain-based company are currently known to be subject to this provision based upon a certified claim and non-certified claim.

Suspension History

Title III was suspended every six months since the Libertad Act was enacted in 1996- by President William J. Clinton (1993-2001), President George W. Bush (2001-2009), President Barack H. Obama (2009-2017), and through the first two years of President Donald J. Trump (2017-2021). President Joseph Biden (2021-2025) suspended again on 14 January 2025. On 20 January 2025, President Donald J. Trump (2025-2029) reversed the suspension.

On 16 January 2019, The Honorable Mike Pompeo, United States Secretary of State, reported a suspension for forty-five (45) days.

On 4 March 2019, Secretary Pompeo reported a suspension for thirty (30) days.

On 3 April 2019, Secretary Pompeo reported a further suspension for fourteen (14) days through 1 May 2019.

On 17 April 2019, the Trump Administration reported that it would no longer suspend Title III.

On 2 May 2019, certified claimants and non-certified claimants were permitted to file lawsuits in United States courts.

Certified Claims Background

There are 8,821 claims of which 5,913 awards valued at US$1,902,202,284.95 were certified by the United States Foreign Claims Settlement Commission (USFCSC) and have not been resolved for nearing sixty years (some assets were officially confiscated in the 1960’s, some in the 1970’s and some in the 1990’s). The USFCSC permitted simple interest (not compound interest) of 6% per annum (approximately US$114,132,137.10); with the approximate current value of the 5,913 certified claims is approximately US$9.2 billion.

The first asset (along with 382 enterprises the same day) to be expropriated by the Republic of Cuba was an oil refinery on 6 August 1960 owned by White Plains, New York-based Texaco, Inc., now a subsidiary of San Ramon, California-based Chevron Corporation (USFCSC: CU-1331/CU-1332/CU-1333 valued at US$56,196,422.73).

From the certified claim filed by Texaco: “The Cuban corporation was intervened on June 29, 1960, pursuant to Resolution 188 of June 28, 1960, under Law 635 of 1959. Resolution 188 was promulgated by the Government of Cuba when the Cuban corporation assertedly refused to refine certain crude oil as assertedly provided under a 1938 law pertaining to combustible materials. Subsequently, this Cuban firm was listed as nationalized in Resolution 19 of August 6, 1960, pursuant to Cuban Law 851. The Commission finds, however, that the Cuban corporation was effectively intervened within the meaning of Title V of the Act by the Government of Cuba on June 29, 1960.”

The largest certified claim (Cuban Electric Company) valued at US$267,568,413.62 is controlled by Boca Raton, Florida-based Office Depot, Inc. The second-largest certified claim (International Telephone and Telegraph Co, ITT as Trustee, Starwood Hotels & Resorts Worldwide, Inc.) valued at US$181,808,794.14 is controlled by Bethesda, Maryland-based Marriott International; the certified claim also includes land adjacent to the Jose Marti International Airport in Havana, Republic of Cuba. The third-largest certified claim valued at US$97,373,414.72 is controlled by New York, New York-based North American Sugar Industries, Inc. The smallest certified claim is by Sara W. Fishman in the amount of US$1.00 with reference to the Cuban-Venezuelan Oil Voting Trust.

The two (2) largest certified claims total US$449,377,207.76, representing 24% of the total value of the certified claims. Thirty (30) certified claimants hold 56% of the total value of the certified claims. This concentration of value creates an efficient pathway towards a settlement.

Title III of the Cuban Liberty and Democratic Solidarity (Libertad) Act of 1996 requires that an asset had a value of US$50,000.00 when expropriated by the Republic of Cuba without compensation to the original owner. Of the 5,913 certified claims, 913, or 15%, are valued at US$50,000.00 or more.

The ITT Corporation Agreement

In July 1997, then-New York City, New York-based ITT Corporation and then-Amsterdam, the Netherlands-based STET International Netherlands N.V. signed an agreement whereby STET International Netherlands N.V. would pay approximately US$25 million to ITT Corporation for a ten-year right (after which the agreement could be renewed and was renewed) to use assets (telephone facilities and telephone equipment) within the Republic of Cuba upon which ITT Corporation has a certified claim valued at approximately US$130.8 million. ETECSA, which is now wholly-owned by the government of the Republic of Cuba, was a joint venture controlled by the Ministry of Information and Communications of the Republic of Cuba within which Amsterdam, the Netherlands-based Telecom Italia International N.V. (formerly Stet International Netherlands N.V.), a subsidiary of Rome, Italy-based Telecom Italia S.p.A. was a shareholder. Telecom Italia S.p.A., was at one time a subsidiary of Ivrea, Italy-based Olivetti S.p.A. The second-largest certified claim (International Telephone and Telegraph Co, ITT as Trustee, Starwood Hotels & Resorts Worldwide, Inc.) valued at US$181,808,794.14 is controlled by Bethesda, Maryland-based Marriott International.